Rabobank global strategist Michael Every is known for his often contrary, frank and sometimes flippant, but always exhaustively researched, opinions. He spoke with Stewart Hawkins about why he’s bearish on this country’s property “obsession”, the economic danger of intergenerational inequity, the continuing threat from China and bemoans the way we constantly do “stupid things cleverly and clever things stupidly.”

This story featured in Issue 13 of Forbes Australia. Tap here to secure your copy.

If you were an Australian with Australian dollar assets, what would be an opportunity, and what would be a danger?

Let’s start with a danger because my personal bias, which is one of the reasons I don’t manage money, is towards not losing any of it before you think about making it. What worries me most in Australia is this continuing, almost religious obsession with property. It’s almost sacrilegious to discuss it, even though a few heretics are allowed to in certain corners, and they’re just ignored or mocked.

The RBA [Reserve Bank of Australia] is not going to be able to cut [rates] anywhere near as much as it wants to, as fast as it would like. A lot of people are

still doing it hard, and just dreaming that everything will get easier within the next couple of months, and it isn’t. That’s already worrying enough at the margin.

I look at Australia through a broader global context because it’s not unique.

Almost everywhere else in the world, you are seeing governments moving against property and understanding that [for] the socio-economic reasons alone, in terms of maintaining any attempt of a middle-class dream and preventing working-class rioting, yeah, in all seriousness. You cannot have a world in which it’s normal to have Sydney, Melbourne, Brisbane, Adelaide, house prices going up 10% year-on-year, and your pay going up 3% because no one can afford it even now. Renters are doing it hard. First-time buyers can’t afford anything, yet the default thinking is, “This is all just a bump on the road and in no time at all, we’re back to double-digit gains, and that’s just the standard.”

As I quip on this, people think I’m flippant, [but] that’s when I’m being my most serious. Project the dots forward in a society where you earn 3% more a year and property goes up 10% from this starting point. When families have to split a house between X number of kids to give them a deposit, which they then can’t leverage up into anything big enough to match the lifestyle they want.

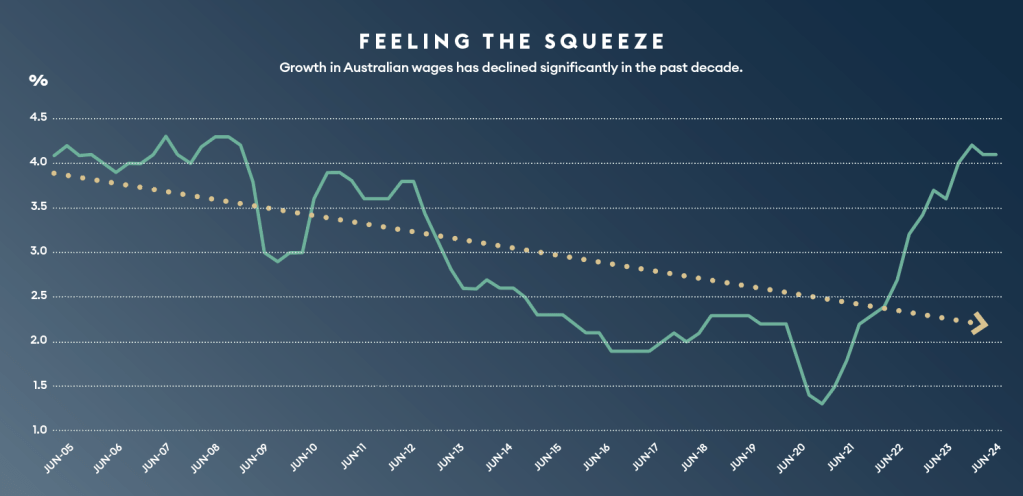

Growth in Australian wages has declined significantly in the past decade. “Project the dots forward in a society where you earn 3% more a year and property goes up 10%,” says Michael Every.

DATA NOTES: All sector WPI, quarterly and annual movement (%), seasonally adjusted. Source: Australian Bureau of Statistics, Wage price Index, Australia June 2024

That’s a feudal system you’re moving back to eventually, where land is all that matters. There is no economy other than the ownership of land, which is concentrated in fewer and fewer hands, and [for] everyone else basically, everything they earn is going to pay someone else’s mortgage.

You’re not far away from that for some already. If that’s the case, you tell me how you keep society together, and I’m deadly serious when I say that, looking at the terrible frictions that we’re getting in various other different economies, which worry me as a human being, not just as an analyst, intensely.

Then you say, we’ll combine that with a big Australian population growth model, which you can see is running into problems in Europe with populism, in the UK with riots and is running into problems in America [and] in Canada because you end up very often with a declining GDP per capita, which I think is also true in Australia, depending on how you look at the data. Definitely the median GDP per capita data.

You’ve got declining median GDP per capita, a property-centric, property-obsessed economy, which will only be accessible to an ever-decreasing circle of people.

I understand, maybe from an Australian perspective rather than the European one, when you say feudalism, it probably doesn’t mean as much to you, because that’s never really been something you’ve experienced in your DNA, but every European understands what it means. You are just there with the Lord over you, and you’re never free.

Is that a story for 2025? No. 2035? No. 2045? Yeah.

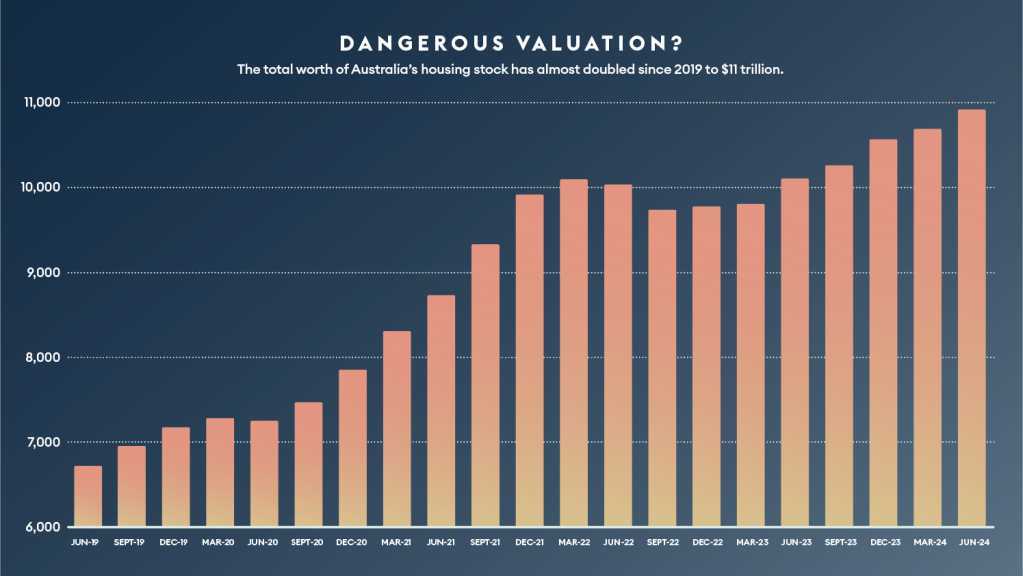

Australia’s housing stock has reached valuations some consider conerning at best, perilous at worst. The latest data from the ABS suggest it’s approaching $11 trillion – four and a half times the estimated annual GDP of the country. Source: Australian Bureau of Statistics, Total value of dwellings June quarter 2024, figures in billions of AUD.

[In the UK] they’re probably going to raise inheritance tax, so you can’t pass your property onto your kids without getting stung, so that mechanism goes. They’re also talking about introducing rent control, so you can’t just whack up rents as much as you want, regardless of supply and demand.

They’re also talking about absolutely murdering you with an annual property tax, so maybe 1% or 2.5%, and then gradually going higher, so just holding on to that property dream means that… [say] you’re a pensioner in Sydney and you bought the house in the 1960s – you’ve got something worth five million Aussie, but you’ve got just a pensioner’s income. Yeah, fantastic, you now owe $50,000 a year in a new property tax just to sit in it.

That overturns the entire apple cart.

Australia may be the last holdout; it could well be. Everyone who’s arriving is working really hard, God bless them, trying to pull themselves up and thinking they’re going to get a fair go while they buy a house 80 kilometres away from the beach in the Blue Mountains and still call it Sydney.

So how do we fix this? What do we do?

The longer you wait, the worse the problem gets. If you’ve read political theory and political history, the last thing you want to do is radicalise your middle class when your working class is already radicalised. That’s when you really get bad political outcomes because you shake up your petite bourgeois, when you’re working class; [you] tend to, historically, get drunk, have a street fight and go home. They don’t tend to topple governments.

I’m from working-class stock myself, so I can say this. If you radicalise your petite bourgeois, who have got dreams of their kids going to a better uni than they did, and getting a nice comfy job and being lucky, shall we say, in the gravy train of the job pyramid, then yeah, things can get ugly fast. It’s an open secret – if you move interest rates past a certain point, where you start getting any serious defaults happening, your entire banking sector is destroyed. You have a 2008 locally. Just look at the size of their mortgage books.

What you need to be targeting, as an official who doesn’t want to blow society up, is to get the message through to everybody, ‘You’ve had a good run. You’ve done very well. That’s no longer our economic model.’ For example, from a government perspective, you get rid of negative gearing.

But if you can’t do that – you countermand it by saying, ‘Capital gains tax goes up on anything other than your first home.’ Let’s start there, and you can move back – and it’s on an increasing scale for third and fourth and fifth investment properties etc, so there is absolutely no juice, there’s no benefit. As you scale up your property portfolio, your profits scale down; there’s just no money to be made in it.

You can use the taxation system to do that. If it wanted to, the RBA could come out and say, ‘Look, house prices are part of our remit’. Financial stability and house prices are part of financial stability. Even when they’re going up, that gives you an artificial Minsky** sense that everything’s good and it’s just building up danger for the future. We would prefer to see house prices move in line with average earnings. That would be something we would like to see going forward.”

As the Reserve Bank, how do you affect that?

You’ve got to do it slowly. You’ve got to do it carefully, but you’ve got to make it clear that is now the game. We’re not going to try to blow you up, but there’s no money to be made in this over time, and the window in which you can make money is going to taper down. You should not be looking to be lucky and should actually invest in something innovative and productive.

How does geopolitics play into this?

The Fed [US Federal Reserve] sets the price of borrowing for everyone. Everyone else in the West pretends they’re independent and follows the Fed, plus or minus a little – a little before and a little bit after, depending on how brave [they] are. You’re like little dogs running around the big dog walking down the street.

Global capital can move freely except in and out of China and North Korea, basically, and countries with sanctions. Within each economy, it can go into whatever sector it wants, and you can arbitrage between under-performing and over-performing sectors to get whatever you want.

We are seeing what the outcome of that free choice looks like, which is everybody wants to invest in short-term, get rich quick Ponzi schemes, arbitrage things like the basis trade, boring little technical things in the market, where you’re just making money from slight differentials between similarly priced assets.

Everybody wants to make money from money, as quickly as possible, or from land and housing, in Australia’s case, and again, you have the tax incentive there.

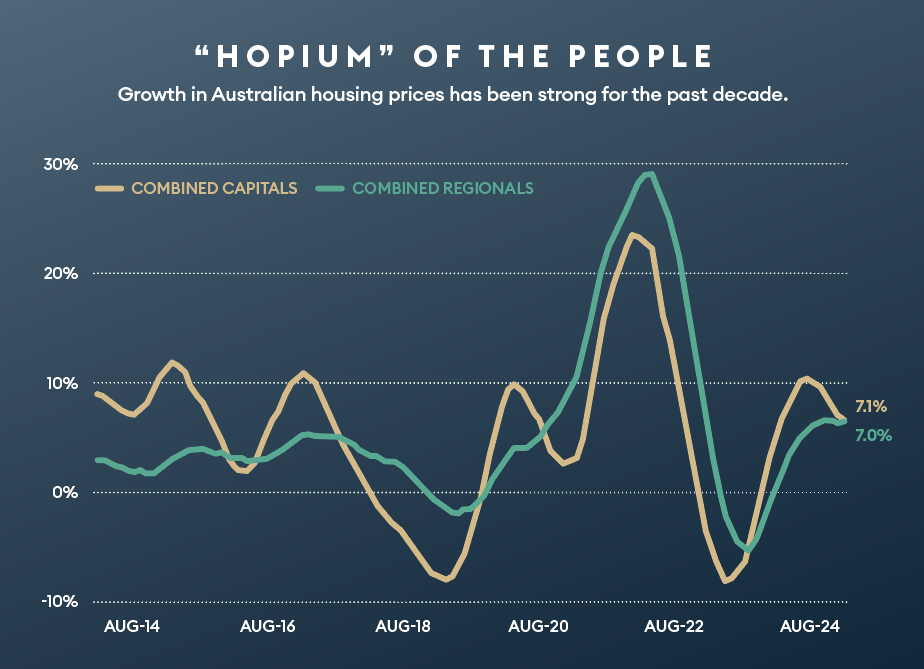

Australia’s almost “religious” obsession with property begins to become understandable –

on paper – when you look at the growth in prices during the past decade – the caveat is “on paper”.

DATA NOTES: Rolling annual change in dwelling values. Source: CoreLogic.

Nobody really wants to invest in innovation or R&D or building a physical company, except tech companies, which themselves generally have the goal of being global monopolists, or making money from other people’s products, which they then act as a platform for.

We do stupid things cleverly, and we do clever things stupidly. It means boom-bust cycles, it means inequality, it means all kinds of problems.

You make great money from money, and corporate profits are up on the back of it, but if you dig into corporate profits, most of it is being made from property or from share buybacks. It’s not being made from innovation or new capital plans, as it should be in a traditional economic model.

We now live in a geopolitical world where 40 years of doing that has generated enough inequality and unhappiness domestically that government after government is getting worried about what their populations will do. How far can we push this before the feudalism really does generate feuds, and when you do get the middle class being left behind to the degree that they side with the working class and say, “Let’s do the rich.”? That’s starting to emerge as a worrying trend – when you get Ivy League students running around radicalised.”

What about Australia and our region specifically?

Australia knows all about this now, the hard way. You have China emerging, and people are realising what I’ve been warning of for a long time: China is not a capitalist economy. It’s a Marxist, Leninist, Maoist, Xi Jinping-thought political economy.

Xi Jinping himself said that this is not a secret. He basically said, ‘Since our bubble burst a few years back, we no longer want property to be frothy. We’re not interested in the property market and how you make money; our homes are for living in.’

You’ve had their stock market shut down because basically they’ve said, ‘We don’t want people making money from shares. We don’t want what they call, and this is Marxist terminology: “Fictitious capital.’ Marx described it in the 19th century – ‘We want productive capital.’ They are Marxists in China; that’s how Xi Jinping sees the world. What he means is, ‘We want money going into physically making things’. That’s where you make money, from widgets, from adding value with your hands or a machine.

The long and short of it is this, you’ve got China running what we call a mercantilist trade model, which is: we sell everything to the world, and we just buy raw materials, and the trade pattern shows that. They don’t even buy many luxuries anymore.

Europe used to sell them luxuries, increasingly, they’re saying, these are not necessary. You [Australia] are basically selling them iron ore, and they’ll buy that from Africa soon rather than from you and Brazil.

You’re at the cutting edge because you’re an extreme example. You’ve really over-specialised.

There is one [response], which is: ‘Okay, we get lower interest rates, higher house prices, forget about the inequality, forget about the feudalism, forget about whether we can or can’t trust China on trade in the long run, it’s all good.’ That’s the “hopium”, which I’m seeing around me.

The geopolitical backdrop [may be] China, turning off raw earths, stopping buying Australian products, wine, beef, lobster. You’ve been on the sharp end of this.

Therefore, if you just surrender without a fight, just give up, and allow [China] to sell us everything, and we become a purely service-based economy with lower interest rates and higher asset prices, over time, we are ultimately beholden to [China]. From an Australian perspective, I know a hell of a lot of people who will sign up for that deal tomorrow, but I can tell you for a fact, that the Americans never will.

Because how do you build your armed forces? How do you have your aircraft carriers if you can’t build them? How do you build your F-35s? How do you sell them if you don’t have any physical supply chain? The Pentagon is so enmeshed in Chinese supply chains that it doesn’t know how deep it is in itself, and it’s panicking; realising it needs to get out of it.

So, what do we need to do next?

We can’t afford to make mistakes. Are we really going to go back to a world of low interest rates, 10% property growth, year on year, speculating on what new app that makes cats look like dogs or dogs look like cats is the new soup du jour?

Or is the government going to start saying, ‘Look, we want to retain a lot of the free market, but there are areas here that are going to take priority. Capital is going to flow to them primarily, and if you want to borrow at 6% or 7% to build an app or want to buy an investment property, go for it, but you’re going to be taxed to the hilt. If you want to do it, it’s a lovely thing to do, but just don’t expect it to be easy money.

No more free money. Free money is going to be for national security or industrial supply chains. It will completely invert your entire demographic, socio-economic, socio-clinical and global trading pyramid. For Australia, it could not shake your overly specialised economy more, because it’s anti-services and pro-industry. It’s anti-exporting – at least to China. It’s pro-Japan, pro-South Korea, pro-Philippines, pro-Vietnam – pro-anyone in the US block.

It means you’re no longer synced with the Chinese economic cycle. You’re back in the dollar block again, where you used to be. It doesn’t matter what the PBOC is doing. Once upon a time, the RBA and the PBOC would’ve been in sync, you’re going to be closer to the Fed again. Does it have opportunity? Oh God, yeah. You’ve got every card in your hand, given that everyone wants to live in Australia. It’s a fantastic place and you’ve got every resource in the world.

Everyone likes you. You are surrounded by growing economies, and not just China, again, many of which are like you. You’ve chosen to stick with the current hegemony in terms of who will defend you and who’s still in front, even if they’re playing their cards badly. Within Australia, yes, you will see a shift back towards industry – you will see a shift away from services.

Rabobank is obviously a huge agri bank in Australia. Naturally, agri is a sector that Australia still needs to be in because there’s no way on earth in which you’ll get out of that sector and just go back to pure industry, [but] it needs to be something that’s higher up the priority list. You think, ‘What could be done if the government spent as much time and the RBA spent as much time thinking about agriculture as it did about housing?’

Now, admittedly, people are worried about, ‘Who are we going to sell to if we can’t sell to China?’ We don’t have a shortage of hungry people in the world. We don’t have a shortage of growing populations in places like Africa. It’s an example of how the government needs to be thinking.

What’s your final piece of advice?

Be the change you want to see in the world. I would spend as much time thinking about my property portfolio as I do about how to use the levers that you have as citizens in a country like Australia to broaden out the discussion to say, ‘How can we create an Australia that’s sustainable in the broadest sense of the term; for all of us?’

**A “Minsky moment” is named after mid-20th century economist Hyman Minsky, who spent much of his working life trying to figure out ways to avoid macro financial crises. Popularly, the term is used to describe a rapid collapse of asset prices usually after a time of smooth conditions and steady growth.

What is fictitious capital, who coined the phrase and what does it mean?

Fictitious capital, a term popularized by Karl Marx, refers to assets that represent claims on future profits. Examples of such are stocks, bonds and derivatives. These contrast ‘real capital’ such as human capital (skill and labour), infrastructure or equipment, which directly contribute to production. If you were left with only fictitious capital, you would have no ability to produce anything. Fictious capital does, however, represent anticipated future cash flows and can be beneficial in spurring investment through the sense of wealth it creates. Fictious capital also elicits the danger

of speculative bubbles, as its very nature is anticipatory. This volatility can also make central banks take monetary or fiscal action which also indiscriminately affects ‘real capital’. – James McCreery

This article represents the views only of the subject and should not be regarded as the provision of advice of any nature from Forbes Australia or Rabobank. The article is intended to provide general information only and does not take into account your individual objectives, financial situation or needs. Past performance is not necessarily indicative of future performance. You should seek independent financial and tax advice before making any decision based on this information, the views or information expressed in this article.