Megan Baldwin has devoted her life to a molecule that could save the sight of millions and make billions for Opthea. In just a few months, the results will reveal if her gamble has paid off.

In the second quarter of 2025, there’ll be a trading halt on Opthea shares. A bunch of people will be locked in a room and the “readout” of the biotech’s first phase-3 trial will come onto a big screen.

If enough of the 1,000 enrolled patients currently going blind with macular degeneration can see an extra line or so of letters on an eye chart, a blockbuster will likely be born. And Megan Baldwin will be vindicated for her decade of grit and grind leading the small, ASX- and Nasdaq-listed Australian biotech developing science that she’d worked on since her PhD in the 1990s, resisting the efforts of big pharma to buy Opthea out.

If the patients’ vision hasn’t been improved in that first trial – and a similar one due months later – Opthea might fade to dust. That $775 million the scientist raised to get it to where it is, plus the $225 million raised by her CEO successor, Frederic Guerard, might all be for nothing.

While they say there are other pathways to market if it fails, Opthea has no drug close in the pipeline other than its OPT-302. As one analyst said, “In a year, Opthea will be either worth $2 [per share] or 10 cents.”

The last time Opthea had a critical “readout” was in 2019 with the phase-2b trial. The patients on OPT-302 could see between 3.4 and 5.7 more letters on the chart than the control group. [The chart has five letters per line.]

Baldwin recalls that “readout” when the woman next to her let out a sigh of disappointment as the results came up on the big screen. Until she realised she read it wrong. “Then she goes, ‘No! No! It hit! It hit!’ We’d hit statistical significance. It was the turn of the card. There’s a point where you didn’t know it worked, and there’s a point where you know.”

Within a month, Opthea’s share price had risen more than 400%, to more than $3.

“No one had done this before,” says Baldwin. “We’d powered the study really well, and we had achieved an outcome that, frankly, large pharmaceutical companies had been unable to achieve.”

Despite the positive results, however, investors lost interest in Opthea as massive hurdles to getting a drug approved became apparent, not least of which was raising hundreds of millions to get it through the next phase of scientific and regulatory hoops. Baldwin fielded the calls of big pharma suitors wanting in on the action, but she fended them off and pressed on. As a result, the company still owns 100% of its IP – 100% of its upside.

“You have the high when you read your result out, and then in about 15 seconds, you start to think about the next thing – the next stage of clinical development. It’s about getting more money in the door.”

Baldwin’s background does not immediately suggest she’d be the right person to get that money through the door, but few people are as heavily invested in the field.

In 1996, when Baldwin was looking for a PhD project, vascular endothelial growth factors (VEGFs) were a newly discovered protein known to play a role in allowing cancers to thrive by promoting vein and capillary growth around the tumours.

Baldwin began mapping the genes of one such protein, VEGF-D, which had just been discovered by professors Marc Achen on and Steve Stacker at the Ludwig Institute for Cancer Research in Melbourne.

Her supervisor there in the early years was Professor Andrew Wilks, who was about to leave the Ludwig and take the then unheard-of step of going private with his own cancer research, which was sold to GSK for $2.8 billion last year. He remembers Baldwin as “really, really smart and driven like no one else I know”.

In 2001, Baldwin went to do post-doctoral work at Genentech in the US, where she worked under the Italian-American molecular biologist Napoleone Ferrara, who had pioneered the VEGF field.

She was there in 2004 when Genentech released Avastin, which became a blockbuster cancer treatment by blocking another VEGF – VEGF-A. Two years later, Genentech repackaged the same drug as Lucentis to treat wet age-related macular degeneration [AMD]. Wet AMD develops when abnormal blood vessels grow into the macula – the part of the retina responsible for high-resolution sight.

In the same way that VEGF-A inhibitors stop excess veins from growing to feed cancer cells, they also stop them from growing in the eye. Genentech suddenly had two multi-billion-dollar blockbusters on its hands.

“During the five years I was there, Genentech grew from a 3,000-person company to about 14,000,” says Baldwin. “It was an eye-opening experience to be in a biotech company that knew exactly where it wanted to be. They were at the forefront of this new sexy research field and they started testing the molecule in different tumour types. They had colorectal cancer, then lung cancer, and it just went on, and the company grew. When you get exposure to that, it fuels your enthusiasm.”

It didn’t hurt that she had a tiny piece of equity.

“It’s a game of resilience – of just getting up and going back to that brick wall and hitting it repeatedly, every day.”

Megan Baldwin

Baldwin moved away from the bench to go into market planning at Genentech before being persuaded to come home, now with husband and baby, to join the ground-breaking Australian biotech Circadian in 2007. [Roche bought Genentech for US$46.8 billion in 2009.]

Circadian had bought the VEGF-D intellectual property from Baldwin’s PhD research from the Ludwig, along with Finnish IP on the related VEGF-C, both of which looked like they could add to the effectiveness of Genentech’s VEGF-A drugs.

As Circadian’s scientific affairs manager, she worked closely with then-CEO Robert Klupacs. It soon became apparent that their molecules worked better on wet AMD than cancer, so Circadian created a new private company, Opthea, with vision as its focus and Baldwin as its CEO.

In 2015, Circadian changed its ASX-listed company name to Opthea [ASX: OPT], with Baldwin as CEO of the new public entity. She had doubters.

“All I heard for the first few years was, ‘You’re a first-time CEO’, and I know other people didn’t get called ‘first-time CEOs’. If you look at the stats, most CEOs are first-time CEOs.”

She put her head down and went to work. They raised $17.5 million at a time when Opthea’s market capitalisation was only $8 million. Investors saw that, as successful as market leader Lucentis was, it still only partly blocked the web of veins forming in the eye. Opthea’s VEGF-D and -C blockers promised to – maybe – block the rest.

The idea was that OPT-302 would not compete with Lucentis. It would be injected with it to complement it and all the other VEGF-A blockers coming on stream. The market grew from $0 to the current $15 billion a year. If Opthea could piggyback just a portion of that, it would have a blockbuster.

The 2017 phase-1 trial of 51 people went well. It was safe, and vision improved above the standard of care. Baldwin raised $45 million to take it through to a phase-2b trial. The share price surged, then sagged.

The 2019 readout came, the share price surged again – by 400%. She raised $50 million, then $192 million, then almost $400 million more. However, it was still not enough to finish the phase-3 trials.

By 2023, the stock had sagged to one-tenth of its 2019 highs.

She was frustrated that people couldn’t understand the magnitude of the undertaking – and the opportunity.

“I think the Australian market expects you to be able to keep generating phenomenal data – but science and clinical development don’t happen like that,” says Baldwin. “It’s a game of resilience – of just getting up and going back to that brick wall and hitting it repeatedly, every day.”

Opthea needed more money. It was going big on the phase-3 trial – two studies with 1,000 subjects each in 30 countries – for maximum statistical power. The team was still only eight to nine staff, plus some contract scientists, when Baldwin raised another $80 million to bring in a US team – a chief financial officer, clinical operations people, and a regulatory person.

She’d raised $775 million by August 2023 and still only had 20 staff.

“As a biotech, I don’t know if you ever exit the valley of death. It’s a tough business, but we’re in a very good place.”

Fred Guerard

And Baldwin was working on a way to put herself out of a job. She says she’d had the expiry-date conversation with the board a decade earlier, even before she took the CEO job – that she’d take it through clinical development. Someone else would take it to market.

A Nasdaq listing and a growing U.S. team meant more time was needed in the States. She didn’t want to live there again. With 18 months before the phase-3 readout, with manufacturing and marketing channels needing to be set up, she knew it was time.

Fred Guerard, a Frenchman who’d graduated with a doctorate in pharmacy, had been convinced by his work with molecules in rats that his future was not at the bench. His post doc was in marketing, and his career took him through various biotechs including a stint living in Sydney for Novartis. He’d risen to be head of ophthalmology with the pharma giant when he left in 2019 to join a start-up tackling macular degeneration with an injectable polymer. It didn’t work out, and he sold out in March 2023 – in time to be approached by Opthea’s head-hunters for the CEO role.

He already knew Opthea’s story, but when he did his due diligence with its data, he jumped at the opportunity to lead the company, joining in October 2023.

Baldwin stepped aside to become a board member and chief innovation officer. [She “retired” from the board in October 2024.]

Guerard came into a company that still only had 20 employees. In April this year, the last patients were enrolled in the first of the phase-3 trials, meaning there was now an end date. In one year, they’d have the data for the first readout. But in June, they announced they needed another $227 million to reach that point. The share price slumped again, bottoming out at 32c before it was announced in July that the money was in the bag and that the second phase-3 trial was also fully enrolled.

“[It] will be one of the biggest phase-3 readouts for an ASX-listed biotech in recent years.”

Thomas Wakim, Bell Potter analyst

“That allowed us to sleep a little bit better, pay a few bills and wait for the data, basically,” says Guerard in a Sydney conference room last September while visiting from his base in the US

The market got back on the bus. The share price has more than doubled from its 2023 lows, and Opthea has been elevated to the ASX 300. But Guerard won’t get ahead of himself. “As a biotech, I don’t know if you ever exit the valley of death,” he says. “It’s a tough business. But we’re in a very good place.”

As far as attaching a value to the company, he says he’d be a very rich man if he could predict such things. “But one way of looking at it is the share price has been chronically depressed because of this financing overhang we removed in June. So, I would not be surprised if our valuation would keep on going up until top-line data, which is not uncommon in biotech. The [wet AMD] market is so big. One percentage point of market share is worth US$100 million of sales a year.”

He is “fairly confident” that OPT-302 will be on sale and in paying customers’ eyes by early 2027. “We need six months to file the dossier with the FDA [U.S. Food and Drug Administration], and then the FDA will take anywhere between six months and a year to review.”

Opthea’s headcount is up to 40, with most of the hires being on the medical side, working with the FDA and cleaning up the data. There’s also a team focused on commercial manufacturing and a PR team – “medical affairs” – out spreading the word to doctors.

Aside from the U.S. being the largest wet AMD market, Europe and Australia take up to a year to negotiate prices with regulators. “That’s why the launch will always be in the US. It’s where you get approved, and don’t waste time on pricing discussions.”

As for Baldwin, she’s proud of having got Opthea to where it is with such frugality. “There’s a lot of pride and ownership around the fact that we’ve created this baby, and the baby’s grown up into a phase-3 asset.” she says. “There’s also a sense of responsibility to ensure we change patients’ lives. And we want a reward for all the investors that come in and support us.”

Baldwin is now also on the investment advisory board of her old professor Andrew Wilks’ biotech venture fund, SYNthesis BioVentures. And while SYNthesis hasn’t invested in Opthea, Wilks has backed Baldwin’s baby with his own money.

“I’ve put a fair amount of cash behind her,” says Wilks. “I think she’s worth backing every step of the way.”

Opthea’s Origins

Opthea grew out of Circadian, a biotech founded by visionary accountant Leon Serry in Melbourne in 1984. A decade before CSL and Cochlear floated, Serry saw that ground-breaking Australian medical research was not getting commercialised.

Circadian went on to incubate such companies as:

Victoria state-founded Amrad, later renamed Zenyth and sold to CSL for $108 million in 2006.

Metabolic, which morphed into ASX-listed Polynovo, with a market cap of $1.55 billion.

Antisense, now Percheron, a long-lived biotech with a crucial phase-2b readout coming this month.

Optiscan, ASX-listed cancer diagnostic company.

Axon Instruments sold for $140m in 2004 and is now headquartered in Silicon Valley.

Circadian dabbled in drugs for Alzheimer’s and cancer, as well as melatonin for jet lag, from which it got its name before it went all in on eye ailments and changed to Opthea.

Serry died, aged 83, in September 2024.

Value-inflection injection

The market for VEGF-A inhibitors in wet age-related macular degeneration is $15 billion a year. Current treatments include Lucentis, Eylea, Beovu, Vabysmo and the cancer drug Avastin, which is used off-label. All are delivered with an injection into the eye.

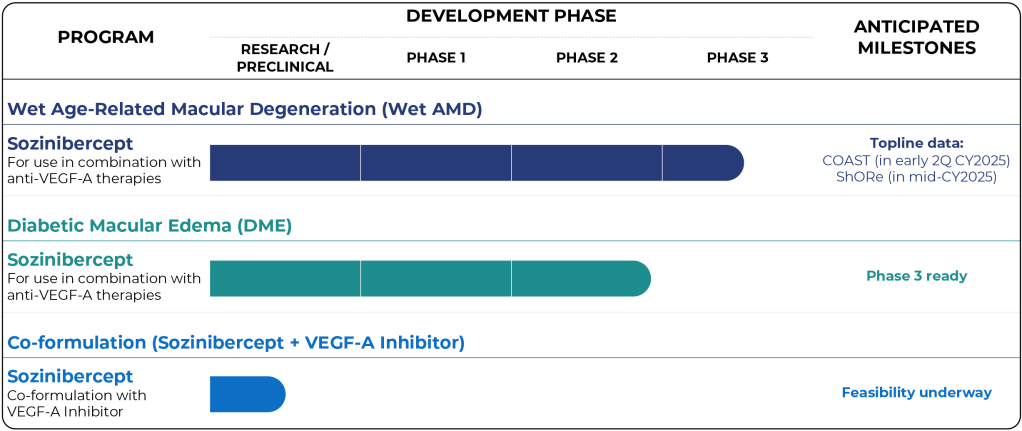

Opthea’s OPT-302 – aka Sozinibercept – is designed to be a second injection to improve the efficacy of all those treatments. It is the only such drug in development. Going on the phase-2b data, it appears most effective in those patients for whom the existing drugs are least effective.

Bell Potter analyst Thomas Wakim describes it as a “blockbuster opportunity”. He put a $1.30 valuation on Opthea shares when they were trading at 71c. [It has since fallen about 10c.] That valuation factors in the considerable risk of the phase-3 trial not going to plan. Other key hurdles are that regulators might not approve it, that Opthea might not raise the capital needed to get to market, and the manufacturing process might not scrub up.

“OPT is financed through to what will be one of the biggest phase-3 readouts for an ASX-listed biotech in recent years,” says Wakim. He styles the readouts as “value inflection points”.

There are 3.5 million people with wet AMD across Australia, the US, Canada and Europe who could benefit from OPT-302.

Bell Potter’s valuation is based on a conservative presumption that it would gain just 10% of the market in four years, worth about US$1 billion in annual sales.

If the Wet AMD trial is successful, the company will pursue phase-3 trials in diabetic macular edema which would open up a market that is almost as large, but growing faster.