With its stock down 80% from its pandemic high and its share of online payments slipping, the fintech pioneer and new CEO Alex Chriss need a win.

The past three years have been tough for PayPal, one of Silicon Valley’s oldest and largest fintech companies, a storied business that counts Elon Musk, Max Levchin, Peter Thiel and Reid Hoffman among its founders and early employees. Its stock has fallen 80% from the $360 billion all-time-high market value it hit in July 2021; the share of ecommerce sales worldwide that flow through its branded PayPal button has been eroding; and some of the company’s recent attempts to rejuvenate its product lineup have gotten little respect from analysts.

In late January, PayPal held an “Innovation Day” conference that new CEO Alex Chriss had promised would “shock the world.” A research report by FT Partners captured investors’ reaction, dubbing the event “Innovationless Day” and writing that the announcements were “largely comprised of uninspiring / recycled advertising methods ranging from placing ads in PayPal receipts and Venmo’s social feed to reorganizing PayPal’s in-app cashback offers.”

Wall Street’s smirks and yawns were likely a harsh reality check for 46-year-old Chriss, who became PayPal’s CEO just last fall after 19 years at Intuit, where he was an executive vice president and oversaw its QuickBooks business. He was brought in to help the 26-year-old San Jose-based company regain its momentum, but it appears that won’t be easy. PayPal declined to make Chriss available to Forbes for an interview, though his predecessor Dan Schulman did talk to us.

PayPal CEO Alex Chriss.

PayPal

Nearly a decade after its spin-off from eBay (which acquired the payments startup in 2002), PayPal still has a profitable franchise, with over $4 billion in net income in 2023. Its digital financial network of 220 million monthly active customers is one of the world’s largest, standing behind juggernauts like Apple Pay and China’s Alipay.

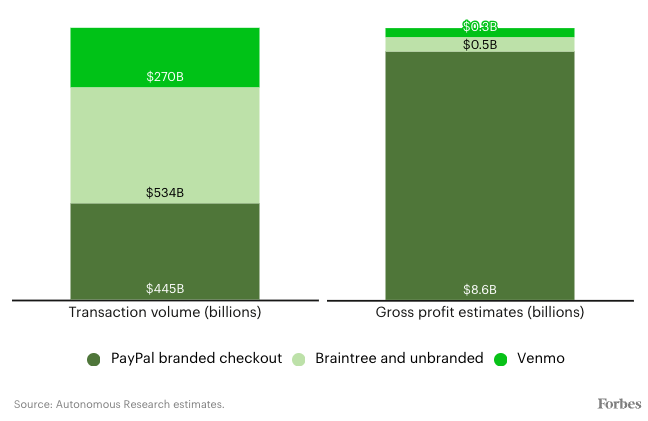

While PayPal has done dozens of acquisitions and entered nearly as many new business lines, more than 60% of its $14 billion in gross profits still comes from the PayPal button, according to Autonomous Research. That’s the icon people click to pay for anything from tchotchkes on eBay or Etsy to diapers from Target. Many users still see it as a safer way to transact instead of trusting an unfamiliar website or person. But transaction growth for PayPal’s branded button is slowing–last year, it grew just 7% in dollar terms, compared with about 9% for ecommerce overall.

From the outside, that button appears largely the same as it did years ago. “The core business is still effectively the cash of the internet–payments 1.0,” says FT Partners managing director Craig Maurer. Part of the problem seems to be that PayPal has long struggled to modernize and integrate disjointed parts of its payments technology. Meanwhile, the risk and fraud-prevention benefits that have buoyed PayPal for so long have ceased to be the competitive advantages they once were, with products like Apple Pay and Shopify’s Shop Pay taking a growing share of the market.

Now Chriss, who was awarded a $42 million pay package by PayPal in 2023 (part of which is contingent on the company’s future performance), is hanging his hat on new strategies, including a “Fastlane” product to speed up guest checkout. But some analysts are skeptical of the impact it will have on profits and think the plan will take much longer to make a difference than investors realize.

Before Alex Chriss took over at PayPal, former American Express executive Dan Schulman ran it for nine years, nearly quadrupling PayPal’s yearly revenue to $30 billion and growing earnings per share from under $1.00 to $3.85, according to FactSet. Yet today, in retrospect, some Wall Street analysts fault Schulman for going in too many directions.

They point to acquisitions that haven’t seemed to pay off, such as iZettle, a Swedish company that makes point-of-sale checkout devices, which PayPal paid $2.2 billion for in 2018, and Hyperwallet, bought for $400 million the same year, which makes payout technology for ecommerce platforms. Honey, a platform that helps website visitors automatically find coupon codes and cash-back offers, cost PayPal $4 billion in 2020.

Dan Schulman was PayPal’s CEO from 2014 to late 2023.

Christie Hemm Klok for Forbes

Schulman, 66, who owns about $40 million worth of PayPal shares, told Forbes some acquisitions have worked out “extraordinarily well” while acknowledging others have done worse than expected. He adds that acquisitions sometimes take longer to create value, noting that Honey is the foundation for a new advertising technology product that PayPal recently announced.

Asked if he took on too many different priorities, Schulman responds: “Every year, we looked at what we were trying to drive and tried to do fewer things, rather than more things. It’s not always easy to do.” He adds, “Alex Chriss is doing an outstanding job coming into the company. One of the big reasons why I left was that I had been there almost a decade. You want somebody coming in thinking about things differently, thinking boldly, seeing where you can leverage what’s already been done.”

Venmo is another actively debated topic in PayPal’s history. In 2013, two years before PayPal spun off from eBay and a year before Schulman took over as PayPal CEO, eBay purchased white-label payment processor Braintree and the upstart peer-to-peer payment app Braintree owned, Venmo, for $800 million. In 2023, Venmo did $270 billion in transactions, according to Autonomous, but the revenue it produces and its margins are anemic compared with PayPal’s main business.

That’s partially because monetization means trying to get customers to use Venmo’s credit card and to use the app like a neobank, for outgoing purchases (as opposed to just transfers within the Venmo system)—two categories where competition is already steep. Meanwhile, PayPal has had trouble integrating Venmo with the core PayPal platform to create synergy.

At his final investor conference in June 2023, Schulman’s response to a question from FT Partners’ Craig Maurer shed light on PayPal’s ongoing challenges to integrate its fragmented payments infrastructure. Schulman said it was a problem he had been working on since he arrived at PayPal in 2014. PayPal alone had four different payment stacks, while Venmo and Braintree each had their own separate payment rails. “The goal, starting eight years ago, was to bring all of these together onto a single modern payment platform,” Schulman said. “It’s like open-heart surgery on us while we’re running a marathon, because it’s our payment-processing stack. It can’t go down for a second.”

The disparate systems made it difficult to scale efficiently and forced a “tremendous” number of engineers to focus on just fixing things, Schulman said. “It’s been a long, hard slog, honestly, on that, but we are finished,” he added, noting that PayPal, Venmo and Braintree were finally on the same payment rails, and the company could “start to do a ton of things that we could not do with that legacy infrastructure that we had in place before, including things like interoperability between Venmo [and] PayPal.”

In essence, it took PayPal eight years to integrate two of its own systems, and in all that time, the company couldn’t accomplish it with its own home-grown tech–they still needed help from a Visa product called Visa+ to supplement the integration. “It was a stunning admission,” Maurer says. Schulman counters today, “It was a very complex, highly detailed migration that needed to be implemented and stress-tested with each piece of the architecture … Without all of that hard work that had to go perfectly, there is no way that PayPal can now innovate on top of a modern tech stack.”

PayPal stopped reporting Venmo’s revenue after 2021, when it was roughly $900 million, likely a sign that growth has languished. Beyond Venmo, the integration challenges may also help explain why PayPal has had trouble maximizing returns from more of its acquisitions.

MAGIC BUTTON

The decades-old PayPal button accounts for a minority of the company’s total transactions but most of its profits. PayPal’s three largest business segments are shown below.

With Braintree, PayPal’s technology that helps companies accept online payments, which competes with fintechs like Stripe and Adyen, it has built a fast-growing business. PayPal’s total unbranded payment processing unit, most of which is driven by Braintree, did $534 billion in transactions in 2023 (compared with $1 trillion for Stripe), up from $299 billion in 2021.

The problem? PayPal has gotten there partly by pursuing a risky strategy of undercutting competitors on price; it only collects about 0.20% of the value of each transaction, compared with 1.5% to 2% for PayPal branded transactions, analysts say. Darrin Peller, a managing director at Wolfe Research, says PayPal has gotten less aggressive on pricing under Alex Chriss and that investors today are largely focused on profitability, which is not Braintree’s strong suit.

Ken Suchoski, an analyst at Autonomous Research, argues Schulman didn’t innovate enough on PayPal’s branded checkout button during his tenure. Schulman, of course, strongly disagrees. He says that during his time as CEO, PayPal made big improvements in areas like speed, number of clicks to make a transaction, features offered and fraud prevention. He notes that PayPal had an “antiquated tech stack” when he took over, and he oversaw an overhaul of its code that allowed it to go from two hundred software updates a year to tens of thousands of annual updates.

PayPal’s share of the $6 trillion global ecommerce market fell from a peak of 8% in 2021 to 7% in 2023, according to Suchoski. Apple Pay, which is likely the fastest and easiest payment method to use in America today due to its integration with the iPhone, has gone from a 0.5% share to 3% in just five years. Shop Pay, Shopify’s payment app that’s also well integrated with its ecommerce ecosystem, has reached a 1% share over the same period, Suchoski says.

During earnings calls and interviews, Alex Chriss has been calling 2024 “a transition year.” He said in April, “We have a plan that will return this company to where it needs to be,” and Wall Street analysts are giving him credit for being more focused than Schulman.

One of the core tenets of Chriss’ plan is Fastlane, a new product that began development under Schulman and aims to make guest checkout–that is, checkout at a site where a buyer isn’t registered–faster. It allows customers not using the PayPal button to save their shipping and credit card information so that when they return for future purchases, they only need to enter their email and a verification code sent to their cell phone.

Chriss has said that 60% of ecommerce transactions are guest checkouts, and nearly 50% of those are typically abandoned. But PayPal has seen a much higher 80% of those who start a guest checkout continue to a purchase in early instances of customers using Fastlane.

Those statistics sound promising, especially since the total addressable market for guest checkout transactions is in the trillions. But since this is an unbranded PayPal product, there’s a big question around how much Chriss will be able to charge merchants for the feature and how much profit it will really drive. “We may get very aggressive on the pricing side when it comes to Fastlane for 2024, because we want to drive adoption,” Chriss said in April. Then he gave a vague assurance regarding profitability: “Rest assured, we’ll be pricing to value over time to ensure that we get the right value from that.”

Initially, analysts expect PayPal will be charging large customers prices similar to what it charges for Braintree, around 0.20%. Then it needs small businesses to sign on, because it can charge them much higher rates per transaction. Add that challenge to the fact that this feature isn’t yet widely available, plus a structural industry shift toward larger merchants, and analysts at Autonomous and FT Partners think it will be years before Fastlane can make a meaningful difference. “If expectations are that Fastlane will have a material impact on the holiday season of 2024, I think that might be too aggressive … It will be the back half of 2025 before we’ll really know if Fastlane is building momentum,” Maurer says.

Others are more optimistic. Mizuho recently upgraded PayPal’s stock from a neutral rating to a buy, with senior analyst Dan Dolev estimating that PayPal will eventually be able to charge 0.70% of each transaction for Fastlane and that the product will add $1 to $1.5 billion to its annual $14 billion in gross profits over the next 18 months or so.

Dolev also says the PayPal button’s market-share losses have stabilized based on Mizuho’s research of web traffic for top retailers. He takes comfort in that trend. “You don’t want it to become a melting ice cube in the oven. Right now, the evidence suggests it’s like a melting ice cube in the fridge. You can live with that,” he says. In a recent research report, he also commented on this apparent leveling-off, saying, “This may mean the worst of share loss to Apple Pay and others is in the past, and is likely already reflected in the stock.”

More bullish analysts like Dolev estimate that PayPal will grow its gross profit by 6% to 7% in 2025 and 2026, while folks like Ken Suchoski–who is the only analyst with an underperform rating on the stock, out of roughly 45 total analysts who cover PayPal, according to Bloomberg–expect gross profit to grow more slowly, at 3% to 4% over the next two and a half years. (Twenty of those analysts have more neutral ratings on PayPal such as “neutral,” “hold” and “market perform.”) It might be encouraging that only one analyst expects the stock to underperform, if it weren’t down so much–it’s off about twice as much as the average public fintech stock over the past 12 months.

Suchoski thinks payments investors can do better by buying stocks like Fiserv and FIS, which, he says, are trading at similar valuation multiples as PayPal, aren’t facing the same competitive pressures and are growing revenues by up to 8% a year. “You can basically buy a business at the same price as PayPal, but they’re delivering on top-line growth, and you don’t have the execution risk of trying to turn this thing around as you do with PayPal.”

Since earlier this year, Alex Chriss seems to have already gotten more conservative—he’s no longer telling people PayPal will shock them. “He’s been trying to set the bar low and then slowly but surely raise it,” says Wolfe Research’s Darrin Peller. “It’s a better way to approach the stock.”

This article was originally published on forbes.com and all figures are in USD.

Are you – or is someone you know -creating the next Afterpay or Canva? Nominations are open for Forbes Australia’s first 30 under 30 list. Entries close midnight, July 15, 2024.

Look back on the week that was with hand-picked articles from Australia and around the world. Sign up to the Forbes Australia newsletter here or become a member here.